April 25, 2024

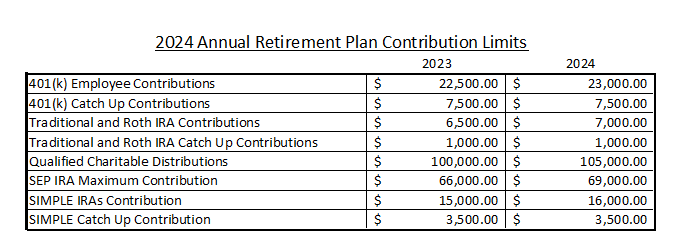

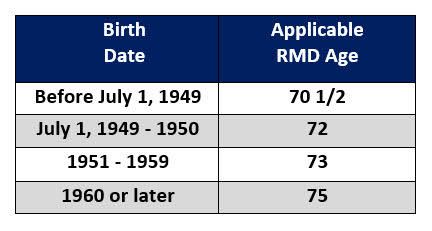

Planning conversations span many topics. One unifying theme, particularly towards the end of the year, is charitable giving. Our goal is to provide you with the knowledge to maximize the benefits of your charitable gifts. Three charitable giving strategies to consider are (1) gifts of appreciated securities from non-retirement accounts, (2) gifts to Donor Advised Funds from non-retirement accounts and (3) Qualified Charitable Distributions from IRAs. For those who do not take required minimum distributions from retirement accounts, gifting appreciated securities or gifting to Donor Advised Funds are great options. For those who take required minimum distributions, QCDs (qualified charitable distributions) should be considered first. The below missive will provide high-level information on each strategy. Tax efficient methods for Charitable Gifts: 1. Gifting appreciated securities directly to charitable organizations – Most individuals make charitable gifts and most of those gifts are made with cash. This year, before writing a check or using your credit card to donate, consider reviewing your portfolio holdings with us. If you have highly appreciated securities, especially positions that are outside our portfolio, you may want to gift shares of stock directly to charity rather than giving cash. By gifting appreciated stock directly to charity, one can avoid selling positions, realizing capital gains, and paying capital gain tax. Charitable organizations are tax exempt. Therefore, the charity can sell the stock without paying tax, keeping more dollars to support their mission rather than the tax authorities. Additionally, for those who itemize their deductions, a deduction may be taken for a percentage of the fair market value of the securities gifted, up to certain limitations. 2. Donor Advised Funds – DAFs are tax efficient vehicles for charitable gifts, particularly for individuals with highly appreciated securities. Like giving appreciated securities directly to charity, gifts to donor advised funds avoid realized capital gains and the subsequent tax liability. One may also take an income tax deduction for gifts to a donor advised fund. The difference between gifts made directly to charity and gifts made to donor advised funds is that the grantor (donor) retains control of the assets in the fund until they are later granted to the 501(c)3 organization of the donor’s choosing. One receives an immediate, upfront income tax deduction for the gift to the DAF but does not receive a deduction when grants are made from the DAF to charity. Donor advised funds are charitable giving accounts that can be used to make future “grants” to qualified 501(c)3 organizations. Gifts to DAFs may remain invested indefinitely and, managed properly, can grow over time. The donor may grant funds out to charities periodically or may designate a charitable organization as the recipient beneficiary at their passing. For individuals who struggle to itemize their income tax deductions, front-loading or “bunching” gifts to a DAF may allow them to itemize in a given year due to the large size of the gift. Instead of spreading out small gifts over several years, donors may consider “bunching” gifts into one year to maximize their income tax deductions or offset a large gain. For example, in a year a business is sold and a capital gain is realized, giving a significant sum to a DAF can offset the realized gains with charitable deductions. Instead of giving a large lump sum to one charity in the same year, DAFs allow donors to make a large gift to the DAF and then subsequently grant many organizations or make grants over many years while maintaining control over the funds in the investment account and allowing the dollars to grow. 3. Qualified Charitable Distributions - QCDs allow individuals to transfer up to $105,000 to charities each year tax free. If the distributions are made directly to the charitable organization, account owners do not owe income tax on the distributions and distributions count towards RMDs. QCDs are a win/win for both the account owner and charitable organization. Account owners can reduce their adjusted gross income by giving directly to charity from IRAs. Gifts are not reported as income and therefore reduce the donor’s adjusted gross income. This can be very helpful for individuals on Medicare because a reduction in AGI may result in a reduced Medicare premium and less tax on social security income. Charitable recipients receive QCDs in full, rather than a reduced amount after federal and state income tax has been withheld. If you plan to make charitable gifts this year and you must take an RMD, consider gifting from your IRA. We will assist you in sending a check from your IRA to the charitable organization of your choice. You cannot be in receipt of the funds; the distribution must go directly from your account to the charitable organization. Frequently Asked Questions How do I know if I need to take an RMD? If you are 73 and you have a non-Roth qualified retirement account, you need to take a required minimum distribution (RMD for short). If you are still employed and have a 401k plan, you will start taking RMDs at age 73 or when you retire (if your plan allows this). We will notify you if you are required to take an RMD and will assist you in taking your distribution before 12/31/24. What types of accounts are considered “qualified retirement accounts”? traditional IRAs SEP IRAs SIMPLE IRAs 401(k) plans 403(b) plans 457(b) plans profit sharing plans other defined contribution plans Can I use a qualified charitable distribution to fund a donor advised fund? No When should I give to a DAF/give appreciated securities from my taxable (non-retirement account) vs. using my QCD? If you are younger than 73 and charitably inclined, consider a DAF (or gifts of appreciated securities) from your taxable account to maximize your charitable giving strategy. If you do not have a retirement account, consider a DAF. If you have retirement accounts and must take RMDs, consider using the QCD since you will get an immediate break on income tax. If your RMD is greater than $105,000 and you want to give more than $105,000 to charity, you may want to consider using both your QCD and a DAF to maximize gifts to charity and minimize your tax liability.